A client recently mentioned that they would soon have to re-brand their newly launched mortgage application.

At first glance, it sounded like a fairly routine request. Re-branding projects are common: update the logo, change the colours, refresh some text and marketing content, and redeploy the application.

What started a much more interesting discussion, however, was my very simple question:

“Why?”

That single question shifted the conversation in an unexpected direction.

What initially appeared to be a straightforward re-theming exercise soon revealed a much bigger strategic opportunity.

Instead of simply repainting the application with a new brand, the organisation began to explore whether they should transform the platform into a multi-brand white-label solution.

What they thought would be a minor update ultimately turned into the beginning of a major digital transformation initiative.

This situation is more common than many organisations realise.

When Re-Branding Isn’t Just About Branding

Re-branding is often treated as a design task. But in many digital platforms — especially in regulated industries such as financial services — branding touches much deeper layers of the system.

In a mortgage application platform, branding can influence:

- Customer journeys and onboarding flows

- Product offerings and lending rules

- Integration with external services

- Compliance messaging and documentation

- Broker or partner experiences

As I explored the client’s situation further, several important factors emerged.

The organisation was planning to:

- Launch new mortgage products under multiple brands

- Partner with broker networks and lenders

- Expand into new distribution channels

- Potentially provide the technology platform to other financial institutions

Suddenly the question was no longer “How do we change the brand?”. It became –“Are we building a single-brand application, or a platform that can support multiple brands?”

That distinction fundamentally changes the architectural strategy.

The Two Paths Organisations Typically Consider

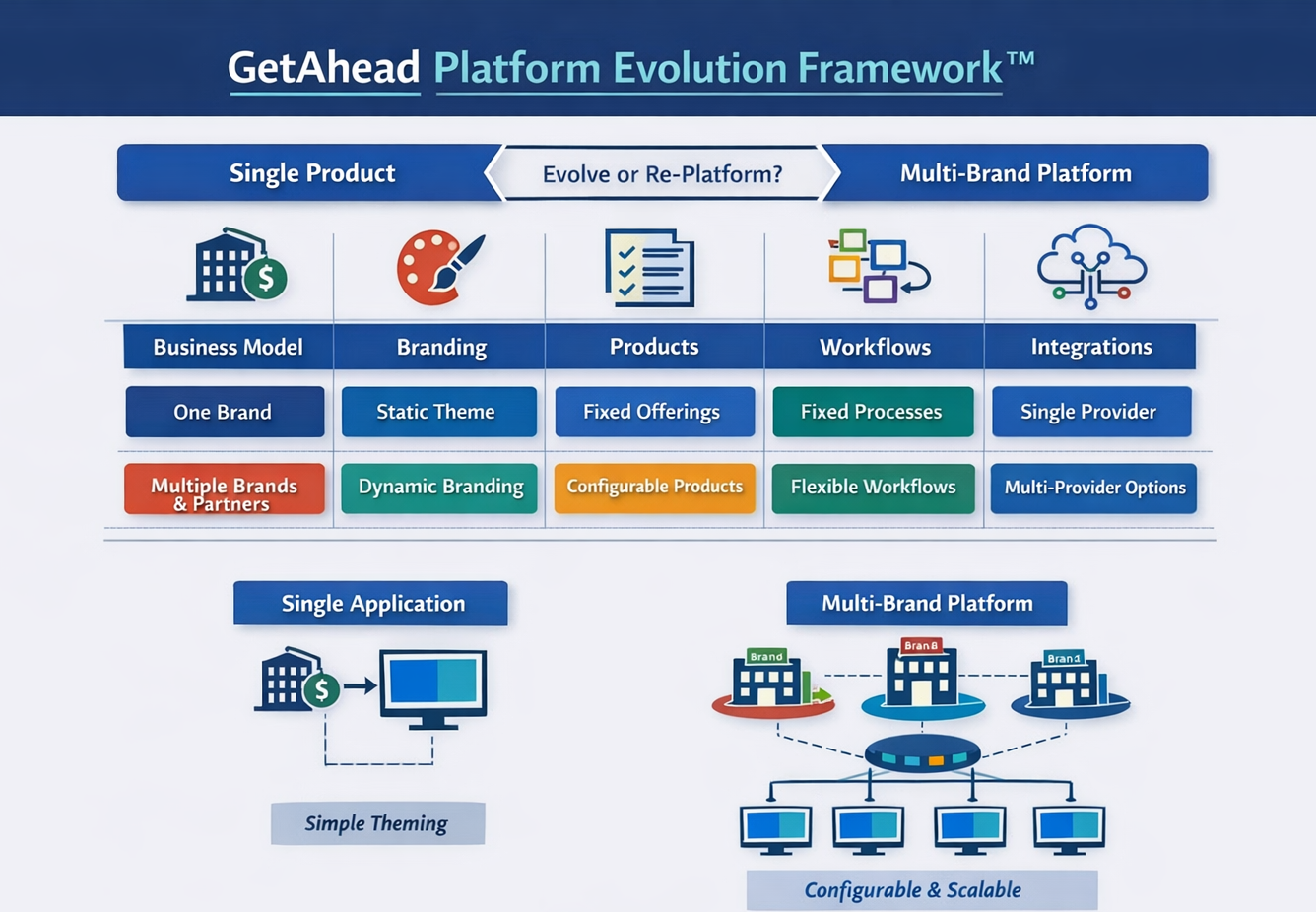

When companies face a re-branding requirement for a digital product, they usually find themselves choosing between two approaches.

Option 1: Re-Theme the Existing Application

The simplest solution is to modify the application’s visual layer.

Typical changes include:

- replacing logos

- updating colour schemes

- adjusting fonts and images

- modifying marketing text

- updating static content

From a technical perspective, this can often be implemented through a theming layer where visual assets are separated from application logic.

This approach works well when:

- the application will still support one organisation

- the products and workflows remain the same

- the branding change is primarily cosmetic

For many companies, this is the right decision.

It is:

- faster to implement

- lower cost

- less disruptive to the existing system

However, during our conversation with the client, it became clear that their situation was more complex.

They weren’t simply re-branding, they were expanding their business model.

Option 2: Build a Multi-Brand Platform

The second approach involves transforming the system into a configuration-driven multi-brand platform.

In this model, the application has a shared core platform, but each brand or partner operates as its own tenant with independent configuration.

Each brand can have its own:

- visual identity

- mortgage products

- workflows and approval rules

- marketing content

- integrations

- compliance messaging

Rather than duplicating applications, the organisation runs one platform capable of supporting multiple brands simultaneously.

This is commonly known as a white-label platform.

White-label architectures are widely used across financial services, including:

- mortgage platforms

- banking apps

- payment systems

- insurance portals

The advantage is that new brands or partners can be launched quickly without rebuilding the system.

But this flexibility requires more thoughtful architecture.

The Real Question: Strategy, Not Branding

The turning point in the discussion came when we reframed the problem.

Instead of asking – “How do we re-brand the application?”

We asked: – “What will this newly re-branded application (or in this case multi-brand platform) need to support in the next three to five years?”

When organisations answer that question honestly, the right architectural path usually becomes clear.

In the client’s case, they expected to support:

- multiple mortgage brands

- partner lenders

- broker distribution channels

- different product configurations

If they simply re-themed the application, every future brand would require:

- new deployments

- custom development

- duplicated infrastructure

- additional maintenance effort

Over time this approach can create technology fragmentation, where multiple slightly different versions of the same system must be maintained.

That scenario quickly becomes expensive and difficult to scale.

What a Multi-Brand Platform Requires

Transforming a single-brand application into a white-label platform does not necessarily mean rebuilding the system from scratch. In fact, most successful organisations evolve toward this architecture gradually.

However, several capabilities typically need to be introduced.

Tenant Management

The platform must support multiple brands as independent tenants.

Each tenant has its own:

- branding assets

- configuration settings

- integrations

- product catalogue

Dynamic Branding

Instead of embedding branding in code, the platform loads brand assets dynamically, allowing each tenant to display its own:

- logos

- colour palettes

- fonts

- marketing content

Product Configuration

Mortgage products often vary by lender. The platform must allow products to be configured rather than hard-coded.

Configuration may include:

- interest rate models

- eligibility criteria

- loan limits

- required documentation

Configurable Workflows

Different lenders may have different approval processes, underwriting steps, or compliance requirements. A flexible workflow engine allows these variations without rewriting the application.

Integration Flexibility

Mortgage platforms typically integrate with external services such as:

- credit bureaus

- identity verification providers

- document signing platforms

- property valuation services

A multi-brand platform should allow these integrations to vary by tenant.

Avoiding the “Big Rewrite” Trap

One of the most common fears organisations have is that moving toward a platform model will require rebuilding the entire system.

In practice, this rarely happens.

Most companies adopt a phased transformation approach, gradually introducing platform capabilities.

A typical evolution might look like this:

- Separate branding from code

Introduce a theming framework for logos and design assets. - Externalise configuration

Move products, content, and settings into configuration tables. - Introduce tenant awareness

Enable the platform to support multiple brands with separate configurations. - Refactor integrations

Convert integrations into modular services that can be configured per tenant.

Over time, the system evolves from a single-brand application into a platform capable of supporting multiple brands.

This incremental approach reduces risk and allows the organisation to continue delivering value during the transformation.

When Re-Theming Is Still the Right Choice

Not every organisation needs a multi-brand platform.

In some cases, re-theming remains the most sensible option.

If the application will continue to support:

- a single brand

- a single lender

- a consistent product set

then introducing multi-tenant complexity may not be justified.

Architecture should always reflect business strategy, not theoretical flexibility.

Turning a Re-Brand Into an Opportunity

For the client in our conversation, the simple question “Why?” changed the trajectory of the project.

What started as a routine branding update became an opportunity to rethink the platform’s role in the organisation’s future.

Instead of treating the mortgage application as a single product, they began to see it as a digital platform capable of supporting multiple brands and partners.

That shift in perspective opened the door to:

- faster partner onboarding

- new revenue models

- scalable growth

Re-branding projects often reveal deeper architectural decisions hiding beneath the surface.

Sometimes the right solution really is a simple re-theme. But sometimes, as in this case, it becomes the catalyst for building something much bigger: a platform designed for the future rather than a product designed for today.

And all it took to uncover that opportunity was one very simple question.

Why?